Why a Quarterly GST Health Check Beats a Year-End Cleanup

GST compliance is not a once-a-year exercise. The Goods and Services Tax Network (GSTN) processes return data every month and runs automated reconciliation across filings. Mismatches between GSTR-1 and GSTR-3B, discrepancies in Input Tax Credit (ITC) claims, and lapses in procedural requirements — e-invoicing, e-way bills, place of supply – are flagged in real time.

When these flags accumulate over four quarters, they arrive as a GST notice with interest calculated at 18% or 24% per annum, penalties, and in serious cases, the reversal of ITC already utilised. A year-end cleanup at this stage is expensive, disruptive, and often incomplete.

A quarterly GST health check — a structured internal audit of your GST records conducted every three months — catches these issues while they are still correctable. Returns can be amended. ITC discrepancies can be investigated and resolved before the annual return locks them in. Procedural gaps can be fixed before they compound.

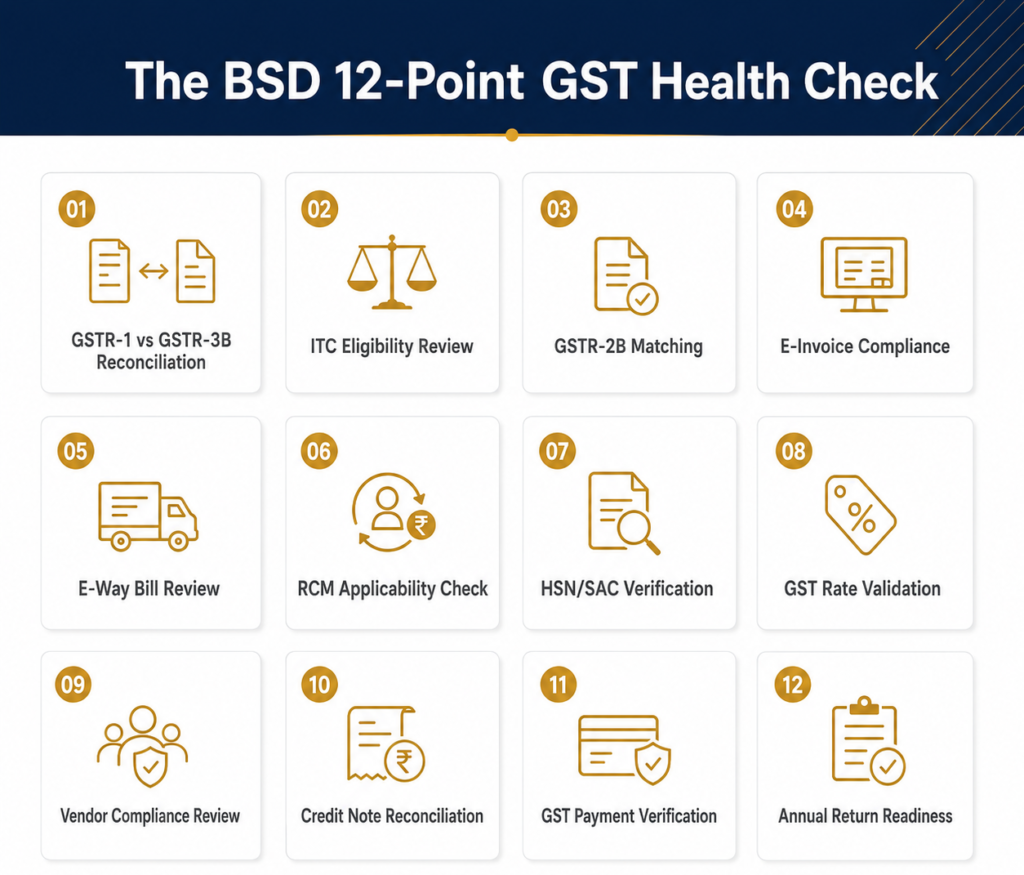

Below is the 12-point framework we use at BSD when conducting GST health checks for our clients. It covers every major risk area from return reconciliation to compliance ratings.

The 12-Point GST Health Check Framework

1. GSTR-1 vs GSTR-3B Reconciliation

GSTR-1 reports your outward supplies (sales) invoice by invoice. GSTR-3B reports a consolidated summary of tax liability and ITC. The GSTN compares these two returns automatically, and any difference — even ₹5,000 — triggers a flag.

Common causes: data entry errors in GSTR-3B, credit notes not reflected in time, amended invoices not captured. Run a systematic reconciliation of total taxable value and tax amounts in GSTR-1 versus GSTR-3B for each month in the quarter. Any delta must be explained and corrected.

2. GSTR-2B vs Purchase Register Matching

GSTR-2B is the auto-drafted statement of ITC available to you, based on your suppliers’ GSTR-1 filings. You can claim ITC only on invoices that appear in your GSTR-2B.

Match your purchase register against GSTR-2B for the quarter. For every invoice where ITC has been claimed but the entry is not in GSTR-2B, investigate: has the supplier filed their GSTR-1? Is there a mismatch in GSTIN or invoice number? If the supplier has not filed, the ITC must be reversed and reclaimed only when the filing is done. Claiming ITC not in GSTR-2B attracts 24% interest on reversal.

3. ITC Eligibility and Blocked Credits Under Section 17(5)

Not all GST paid on purchases is eligible for ITC. Section 17(5) of the CGST Act specifically blocks ITC on certain categories, including:

- Motor vehicles (unless used for specified purposes — transportation of persons with capacity > 13, goods transportation, or training)

- Food and beverages, outdoor catering, health services (unless in the same line of business)

- Club memberships, recreational services

- Works contract services for immovable property construction

- Personal consumption items

Run a check on all ITC claimed during the quarter against Section 17(5). Any blocked credit claimed is a compliance exposure that will need to be reversed with interest.

4. Reverse Charge Mechanism (RCM) Coverage

Under RCM, the recipient — not the supplier — is liable to pay GST. Many SMEs miss RCM obligations entirely, especially on services like:

- Legal services from advocates

- Goods Transport Agency (GTA) services where the GTA has not opted to pay GST

- Import of services (any service received from a foreign entity)

- Sponsorship services

- Security services (where the recipient is a registered body corporate)

Check all vendor payments in the quarter and identify any that fall under RCM. Ensure RCM liability has been declared in GSTR-3B and that the corresponding ITC (where eligible) has been claimed. RCM notices typically arrive 2–3 years after the event, with full interest.

5. E-Invoice Generation and the 30-Day Rule

For businesses with aggregate turnover above ₹5 crore (and progressively lower thresholds as mandated), e-invoices must be generated on the Invoice Registration Portal (IRP) before the invoice is issued to the customer — or within 30 days of the invoice date.

Invoices not e-invoiced within 30 days are invalid for ITC purposes at the recipient’s end. They also expose you to penalties. Audit your invoice register for the quarter: were all B2B invoices registered on the IRP within the 30-day window? If not, what is the exposure?

6. E-Way Bill Compliance

E-way bills are mandatory for the movement of goods where the consignment value exceeds ₹50,000. Check that e-way bills were generated for all qualifying dispatches and that the validity period was not exceeded during transit. Also verify that the e-way bill details — vehicle number, transporter ID, invoice value — match the corresponding invoice.

Unmatched or missing e-way bills are a common trigger for detention of goods and penalty notices during GST audits and inspections.

7. HSN/SAC Code Accuracy

From April 2021, businesses with turnover above ₹5 crore must report HSN codes at the 6-digit level; others at 4 digits. The HSN/SAC code determines the applicable tax rate and is cross-verified by the GSTN.

Audit a sample of invoices from the quarter. Are the HSN/SAC codes accurate for the goods or services supplied? Are the corresponding tax rates applied correctly? Misclassification can result in tax shortfall notices or ITC reversals at the recipient’s end.

8. Place of Supply Correctness

The place of supply determines whether a transaction is intra-state (CGST + SGST) or inter-state (IGST). Errors in place of supply are common — particularly for services with complex determination rules (B2C digital services, construction, transport, intermediary services).

An intra-state transaction incorrectly treated as inter-state (or vice versa) results in the wrong tax being paid and collected. The recipient cannot claim ITC on the wrong head. Both parties will need to file rectifications, and in some cases, the wrong tax collected must be refunded and the right tax paid — a process that can take months.

9. GSTR-9 / 9C Reconciliation Preparation

GSTR-9 (annual return) and GSTR-9C (reconciliation statement, for turnover above ₹5 crore) require you to reconcile data across all 12 months of GSTR-1, GSTR-3B, and your audited financial statements.

If you wait until the end of the year, this reconciliation becomes a massive exercise with months of data. Quarterly health checks make GSTR-9 preparation far simpler: by December, you already have a clean Q1, Q2, and Q3 reconciled. Only Q4 remains.

10. Refund Tracking

If you have accumulated ITC due to zero-rated exports or an inverted duty structure, ensure that refund applications have been filed correctly and tracked to resolution. Refund applications that are not followed up lapse after two years from the relevant due date.

Also verify that any refund already received has been correctly accounted for — refunds credited to the wrong bank account or reversed by the department need prompt action.

11. Late Fees and Interest Exposure

Calculate the late fee exposure for the quarter. GSTR-1 late filing attracts ₹50 per day (₹20 per day for nil returns), capped at ₹10,000. GSTR-3B late filing attracts the same fees plus interest at 18% per annum on tax due. For businesses with high turnover, a single month’s delayed GSTR-3B can result in significant interest exposure.

Identify all late filings during the quarter, compute the interest and late fee liability, and ensure it has been paid before the department raises a demand.

12. GST Compliance Rating Monitoring

The GSTN assigns a compliance rating to each taxpayer based on filing history, reconciliation scores, and other parameters. While the formal rating system has not been fully deployed, the department uses compliance history extensively during audit selection and refund processing.

Maintain a clean filing record. Even one missed GSTR-1 or GSTR-3B affects your reconciliation scores and can delay refund processing. Quarterly health checks ensure there are no inadvertent gaps.

Tools and Templates for Self-Audit

Most businesses can run a basic GST health check using:

- GSTN portal data exports: GSTR-1, GSTR-3B, GSTR-2B, and GSTR-9 data can be downloaded in JSON or Excel format directly from the GST portal.

- Purchase register in Excel or ERP: Match against GSTR-2B exports on a monthly basis.

- IRP (Invoice Registration Portal): Download e-invoice logs to match against your invoice register.

- ERP GST modules: Tally, Zoho Books, SAP, and most ERP systems have built-in GSTR-1 vs GSTR-3B reconciliation reports.

BSD provides clients with a structured quarterly reconciliation workbook that integrates all three data sources and flags exceptions automatically. Ask us for a copy.

When to Bring in an External GST Auditor

A self-audit is effective for routine reconciliation. However, certain situations warrant bringing in an external CA for a formal GST audit:

- Turnover above ₹5 crore (GSTR-9C mandatory)

- Receipt of a GST notice or scrutiny communication

- Significant ITC accumulation awaiting refund

- Complex supply structures — multi-state operations, job work, export of services

- M&A, restructuring, or any change in business structure

- First GST audit after business commencement

How BSD Conducts GST Health Checks for Clients

At BSD, our quarterly GST health check covers all 12 points in this framework, delivered as a structured report that identifies exceptions, quantifies exposure, and recommends corrective actions. For clients with multi-state registrations, we run the check across each GSTIN.

Our process: download and reconcile all return data → match against client’s books → identify and categorise exceptions → compute interest and penalty exposure → recommend amendments and process corrections.

The result: by the time GSTR-9 is due in December, our clients have a clean annual record with no year-end surprises.

Want to ensure your GST house is in order before the next filing cycle? Book a GST health check with BSD. Call 080-4851 7108 or visit bsdgroup.in.