India’s FDI Landscape – Why Foreign Capital Keeps Choosing India

India has consistently ranked among the top five global destinations for foreign direct investment over the past decade. The country received over USD 70 billion in FDI inflows in FY 2023-24, with inflows from Japan, the US, Mauritius, Singapore, and the Netherlands constituting the largest share. Sectors attracting the most capital include technology, pharmaceuticals, manufacturing (driven by the PLI schemes), financial services, and renewable energy.

The structural appeal is well understood: a large and growing domestic market, a competitive cost base, a robust talent pool, and increasingly business-friendly regulatory reforms — liberalised FDI limits across most sectors, streamlined approval processes, and RBI’s ongoing simplification of FEMA regulations.

But for the foreign investor or Indian company raising foreign capital, the regulatory framework governing FDI remains detailed and must be navigated carefully. Non-compliance with FEMA reporting requirements — even inadvertent non-compliance — attracts compounding penalties. Structural choices made at entry are difficult to unwind later. And sector-specific caps and conditions can be opaque.

This guide provides a practical overview of the FDI framework in India: the two investment routes, FEMA compliance obligations, pricing and valuation requirements, entry structure options, and the common pitfalls we see in cross-border transactions.

The Two Routes – Automatic vs Government Approval

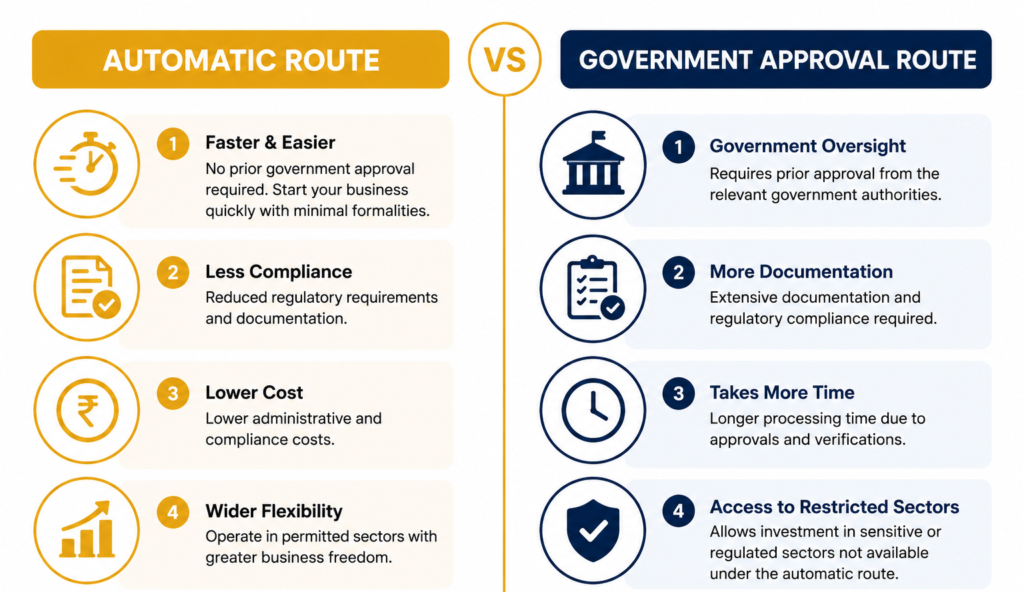

Foreign direct investment in India comes through one of two routes:

Automatic Route

Under the automatic route, a foreign investor or Indian company does not require prior approval from the Government of India or the Reserve Bank of India before receiving or making the investment. The investment can proceed based on the applicable sectoral caps and conditions, with post-investment reporting to the RBI.

The automatic route covers the vast majority of FDI in India — technology, manufacturing, logistics, hospitality, real estate development, financial services (with conditions), and many others. Most private equity and venture capital investments into Indian startups, most Japanese and US manufacturing JVs, and most greenfield investments fall under the automatic route.

Government Route

Certain sectors and activities require prior approval from the relevant ministry or department through the Foreign Investment Facilitation Portal (FIFP). These include:

- Defence (FDI above 74%)

- Broadcasting (content services)

- Print media

- Multi-brand retail trading

- Banking (private sector, above 74%)

- Satellites (establishment and operation)

FDI in sectors not included in either route (i.e., prohibited sectors) is not permitted at all. Prohibited sectors include gambling and betting, lottery, chit funds, Nidhi companies, and real estate business (as distinct from real estate development).

FEMA Compliance Essentials for Inbound FDI

Once an investment is made under the automatic or government route, a series of regulatory reporting obligations arise under the Foreign Exchange Management Act 1999 (FEMA) and the Foreign Exchange Management (Non-Debt Instruments) Rules 2019. Failure to meet these obligations — even if the underlying investment is fully legitimate — attracts penalties under FEMA that compound daily.

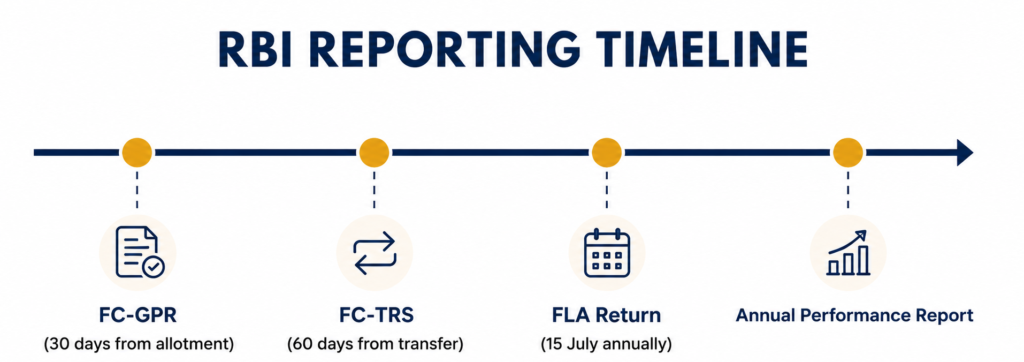

Form FC-GPR – Foreign Currency Gross Provisional Return

Form FC-GPR must be filed by the Indian company with the RBI (through the FIRMS portal) within 30 days of issuing shares or other securities to the foreign investor. It captures:

- Details of the Indian company and the foreign investor

- The type and number of instruments issued (equity shares, compulsorily convertible preference shares, compulsorily convertible debentures)

- The consideration received and the exchange rate applied

- Valuation certificate confirming the issue price meets FEMA pricing guidelines

This is not optional. The RBI will not treat the investment as FEMA-compliant until the FC-GPR is filed and acknowledged. Many companies overlook this when the investment is made quickly under deadline pressure — and then face compounding penalties months later when the gap is discovered.

Form FC-TRS – Transfer of Shares

Form FC-TRS is required when shares are transferred between a resident and a non-resident (in either direction) — a foreign investor buying shares from an Indian shareholder, or an Indian buyer acquiring shares from a foreign investor.

FC-TRS must be filed within 60 days of receipt of consideration (for transfer by a resident to a non-resident) or within 60 days of receipt of funds into India (for transfer by a non-resident to a resident). The onus is on the resident party in each case.

Secondary transactions — secondary share sales, buybacks involving foreign shareholders, ESOP exercises by foreign parent company employees — all trigger FC-TRS obligations.

Annual Return on Foreign Liabilities and Assets (FLA)

The Annual Return on Foreign Liabilities and Assets (FLA Return) must be filed by every Indian company or LLP that has received FDI or made overseas direct investment (ODI), even if no transaction occurred during the year. It is filed on the RBI FLAIR portal by July 15 each year (for the financial year ended March 31).

The FLA Return captures the stock of inward and outward foreign investment as of March 31, along with inflows, outflows, and valuation changes during the year. It is a balance sheet-level disclosure, not a transaction-level one.

Non-filing attracts a penalty of ₹20,000 plus ₹5,000 per week of delay. For companies with large foreign shareholding, compounding applications are expensive and time-consuming.

Reporting Timelines and Penalties

FEMA violations — late filing, non-filing, or incorrect pricing — are handled by the Enforcement Directorate (ED) and the Adjudicating Authority. The penalty under FEMA Section 13 can be up to three times the amount involved in the contravention, or up to ₹2 lakh where the amount cannot be quantified, plus ₹5,000 per day for continuing violations.

The RBI’s Compounding of Offences Scheme allows companies to voluntarily approach the RBI to compound (settle) FEMA violations before they escalate to the ED. Compounding attracts a fee but provides closure. Many companies use the compounding route to regularise historical non-compliance discovered during due diligence for a new investment round or an M&A transaction.

Pricing Guidelines and Valuation Requirements

FDI pricing is not freely negotiable. FEMA imposes minimum and maximum pricing floors depending on the direction of the transaction:

- For issue of shares by an Indian company to a foreign investor: The issue price must not be less than the fair value determined by a SEBI-registered Category I Merchant Banker or a Chartered Accountant using internationally accepted valuation methodology (typically DCF for unlisted companies). The Indian company cannot issue shares to a foreign investor at a discount to fair value.

- For transfer of shares by a resident to a non-resident: The transfer price must not be less than the fair value (same methodology). The resident cannot sell shares to a foreign buyer below fair value.

- For transfer of shares by a non-resident to a resident: The transfer price must not exceed the fair value. The resident cannot pay more than fair value to a foreign seller.

Valuation must be done by a qualified professional — a CA for unlisted companies (under merchant banker category where required). The valuation report must be contemporaneous (at or near the transaction date) and must use an internationally accepted methodology. Standard NAV-based valuations are not accepted for FEMA purposes.

Sector-Specific Conditions and Caps

Even within the automatic route, many sectors carry conditions that must be satisfied:

- Single-brand retail: 100% permitted under automatic route, but the entity must source 30% of the value of goods sold from India (mandatory after 3 years for entities with more than 51% FDI).

- Insurance: 74% permitted under automatic route, subject to ownership and control remaining with Indian residents.

- Telecom: 100% under automatic route for most services; subject to licensing and security conditions.

- Pharmaceuticals: 100% under automatic route for greenfield; brownfield above 74% requires government approval.

- E-commerce: FDI is permitted only in marketplace-based models, not inventory-based. A marketplace entity cannot exercise control over inventory or influence pricing.

Sector conditions change periodically through Press Notes issued by the Department for Promotion of Industry and Internal Trade (DPIIT). Always verify the current applicable conditions before closing an investment.

Choosing the Right Entry Structure

A foreign entity entering India can do so through several structures, each with distinct regulatory, tax, and operational implications:

- Wholly Owned Subsidiary (WOS): A private limited company incorporated in India with 100% foreign shareholding. Full operational control. Subject to Indian corporate tax rates (22% for domestic companies, with surcharge and cess). Most common structure for market entry.

- Joint Venture (JV): An Indian company with a mix of Indian and foreign shareholders. Preferred when local expertise, distribution networks, or regulatory approvals (licences, permits) held by the Indian partner are essential.

- Liaison Office (LO): Can only represent the parent company and cannot undertake commercial activities in India. Funded entirely by inward remittances. Suitable for market exploration, not operations.

- Branch Office (BO): Can undertake limited business activities — export/import, professional services, research — but cannot undertake retail trading or manufacturing. Taxed as a foreign company (higher rates). Requires RBI approval.

- Project Office (PO): A temporary presence to execute a specific project in India. Must be linked to a contract with an Indian entity. Permitted only for the duration of the project.

For most manufacturing, technology, or services businesses entering India, the WOS structure under the automatic route is the most practical and tax-efficient choice. JVs are preferred where sector conditions require Indian partner control or where the Indian partner brings critical non-replicable assets.

Common Pitfalls We See in Cross-Border Deals

Over the years, our team at BSD has seen certain errors recur across inbound FDI transactions. The most consequential ones:

- Not filing FC-GPR within 30 days: Often happens when the investment closes near a holiday or quarter-end. The 30-day window is strict. Set internal reminders the moment funds are received.

- Incorrect valuation methodology: Using book value or previous round valuations for FEMA purposes without a fresh valuation report. Each issuance or transfer requires a contemporaneous report.

- Missing FC-TRS on secondary transactions: ESOP exercises by foreign parent employees, inter-investor secondary sales, and buybacks involving foreign shareholders all trigger FC-TRS. Many are missed because legal counsel is not involved.

- FLA Return not filed: Companies that received FDI in prior years and completed no new transactions assume no filing is needed. The FLA is mandatory every year, regardless of activity.

- Pricing below fair value: A foreign investor agreeing to a ‘discount round’ — below the last-round valuation — without a fresh FEMA valuation report creates a pricing violation.

- Incorrect sector classification: Some businesses operate across multiple sectors. An e-commerce company that also holds inventory may inadvertently violate the marketplace-only FDI condition.

How BSD Handled a Recent Japanese FDI Engagement

Note: All client details in the following case study have been anonymised.

A Japanese manufacturing company approached us through a mutual contact to support their entry into the Indian market through a joint venture with a Bengaluru-based biotech company. The JV structure involved a Japanese entity holding 74% of an Indian private limited company, with the Indian partner holding 26%.

The engagement covered:

- FEMA analysis and confirmation that the applicable sector fell under the automatic route at the 74% level

- Structuring the JV agreement to satisfy FEMA’s ownership and control conditions, given the Indian partner’s minority stake

- Coordinating the valuation of the Indian entity at the time of the JV formation — required for both the FC-GPR filing and for income tax purposes (Section 56(2) fair market value)

- Preparing and filing the FC-GPR within 30 days of share allotment

- Advising on the Indian company’s ongoing FEMA obligations — FLA return, subsequent share transfer reporting, and RBI intimation requirements for any change in shareholding

- Setting up the Indian entity’s accounting and statutory compliance framework — appointment of statutory auditor, ROC filings, advance tax calendar

The transaction closed within the client’s timeline, and the Indian company’s first FLA return was filed on time. The Japanese parent’s corporate team subsequently used our structure memo as a reference for their India entry framework document.

Planning an India entry, raising foreign capital, or navigating FEMA compliance for an existing FDI structure? Our team at BSD brings 53 years of practice and direct experience with cross-border engagements. Call 080-4851 7108 or visit bsdgroup.in to schedule a consultation.