Why Pre-Filing Preparation Determines Filing Outcomes

Every year, thousands of taxpayers file their Income Tax Returns in July under deadline pressure — and pay for it in August, September, or even the following year, when income tax notices arrive for mismatched data, unreconciled income, or missing disclosures.

The Income Tax Department’s systems have grown significantly more sophisticated. The Annual Information Statement (AIS), Taxpayer Information Summary (TIS), and Form 26AS together create a detailed picture of your income from dozens of sources – salary, interest, dividends, capital gains, property, foreign assets, and more. If your ITR does not reconcile cleanly with these statements, discrepancies are flagged automatically.

The fix is not to file faster. It is to prepare better — before you open the ITR form. A disciplined 30-to-60-minute pre-filing review eliminates the most common errors and dramatically reduces the risk of a notice.

This checklist covers what every taxpayer — salaried, self-employed, or HNI — should verify before submitting their return for FY 2025-26 (Assessment Year 2026-27).

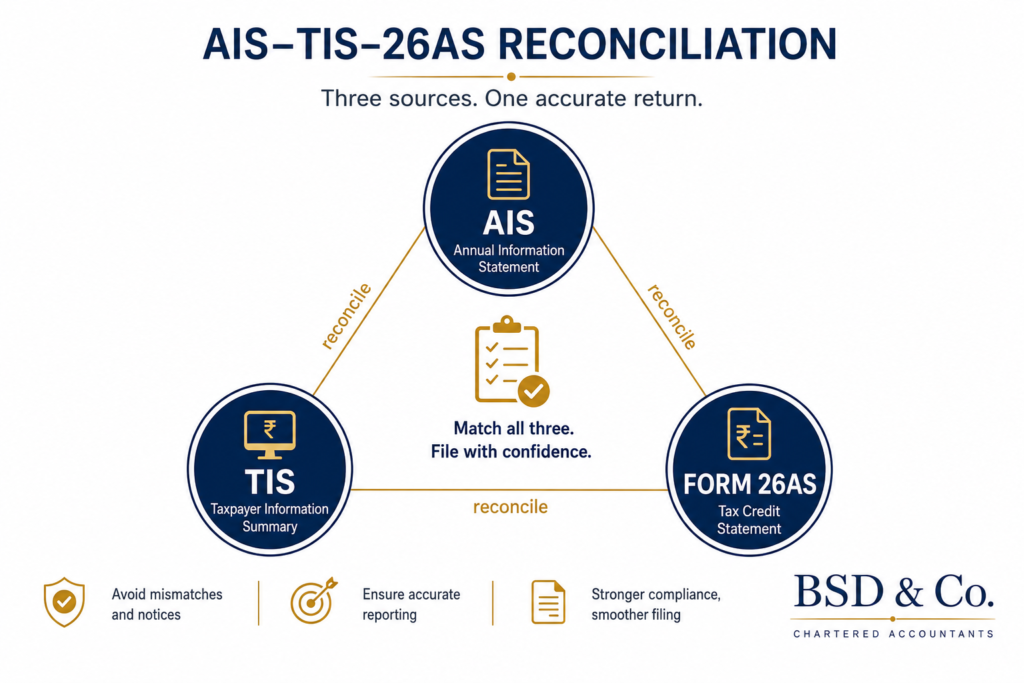

The Foundation: AIS, TIS, and Form 26AS Reconciliation

Before anything else, download and reconcile three documents from the Income Tax Portal:

• Annual Information Statement (AIS): The most comprehensive statement. It reflects income reported to the tax department by banks, brokers, mutual fund houses, employers, registrars, and foreign remittance processors. It covers salary, interest, dividends, capital gains (securities, property), rent received, and more.

• Taxpayer Information Summary (TIS): A summarised version of the AIS, aggregated by income category. It shows the ‘processed value’ that the department will use in pre-filled ITRs if you do not override it.

• Form 26AS: The legacy tax credit statement. Still important — it shows TDS deducted and deposited by your employer, bank, or any other deductor, and advance tax / self-assessment tax paid.

These three will not always match each other — or your own records. The AIS captures reported figures; your bank statements capture actual credit. Reconcile all three before filing. If there are errors in the AIS (incorrect amounts, duplicates, income not belonging to you), raise a feedback directly on the AIS portal and retain documentation.

Key principle: File based on your actual income, not just what the pre-filled ITR shows. The pre-fill is a starting point, not a verified figure.

Income-Specific Pre-Checks

Salary Income — Form 16 Verification, Perquisites, ESOPs

Form 16 is issued by your employer and is the primary source document for salary income. Before filing:

• Match the gross salary in Part B of Form 16 against your salary slips for all 12 months.

• Verify Section 17(1), 17(2), and 17(3) breakdowns — basic pay, perquisites (car, accommodation, ESOP), and profits in lieu of salary respectively.

• If you were allotted or exercised ESOPs during FY 2025-26, ensure the perquisite value (fair market value minus exercise price, on exercise date) is correctly reflected in Form 16 and reported in the ITR.

• If you changed jobs during the year, collect Form 16 from both employers. The new employer may not have consolidated your previous salary for TDS. You will need to compute tax on the combined income and pay any shortfall.

• Check 80C, 80D, and HRA claims in Part B. Verify that the figures match the actual proofs you have — do not claim deductions you cannot support if asked for scrutiny.

Capital Gains — Equity, Mutual Funds, Property, Crypto

Capital gains reporting is one of the most error-prone sections of an ITR. The AIS will capture capital gains reported by brokers and registrars, but your own capital gains statement may differ due to cost basis calculation differences, bonus shares, rights issues, or corporate actions.

• Equity shares and equity mutual funds: Download the consolidated capital gains statement from your broker and from CAMS/KFintech (for mutual funds). Reconcile with AIS. Ensure you have correctly classified gains as short-term (STCG) or long-term (LTCG) based on the holding period.

• Debt mutual funds: With the amendment effective April 2023, debt funds purchased after March 31, 2023 are taxed at slab rates without indexation. Funds purchased before April 1, 2023 have transitional treatment — verify with your CA.

• Property: If you sold property during FY 2025-26, ensure the sale consideration and the stamp duty value are reconciled. Compute indexed cost of acquisition correctly. Section 54 / 54F reinvestment exemption claims must be backed by documentation.

• Crypto and virtual digital assets: All VDA transactions attract 30% tax on gains, with no deduction except cost of acquisition. No loss set-off is permitted against other income or other VDA gains. Ensure every transaction is reported.

Business and Professional Income – Books, Audit, Presumptive

If you are a business owner or professional:

• Ensure your books of accounts are up to date for FY 2025-26. Bank statements, cash book, and ledgers should be reconciled.

• If your turnover exceeds ₹1 crore (businesses) or ₹50 lakh (professionals), a tax audit under Section 44AB is mandatory. Engage your CA well before the September 30 deadline.

• If you are opting for presumptive taxation under Section 44AD (8% / 6% of turnover) or 44ADA (50% of gross receipts), verify eligibility and ensure you have not opted out in any of the preceding five years (for 44AD).

• GST turnover and income tax turnover may differ (e.g., exempt supplies, composition scheme). Reconcile explicitly.

Other Sources — Interest, Rental, Dividends

These are frequently under-reported because income comes from multiple, often forgotten sources:

• Savings account interest: Taxable above ₹10,000 (₹50,000 for senior citizens under 80TTA/80TTB). Collect statements from all banks, including inactive accounts and joint accounts.

• Fixed deposits and recurring deposits: Interest is taxable on an accrual basis, not receipt. Verify TDS deducted (Form 26AS) and compute accrued interest for the year.

• Dividends: Listed company dividends are now taxable in the hands of the shareholder. The AIS will capture dividends reported by companies. Verify against your demat account statements.

• Rental income: Net annual value after municipal taxes and standard deduction of 30% is taxable. If you have a home loan on the rented property, interest deduction is available without the ₹2 lakh cap applicable to self-occupied property.

Deductions Documentation Checklist

Having claimed deductions is not sufficient — you must have the documentation to support each claim in the event of scrutiny. Assemble the following before filing:

• Section 80C (up to ₹1.5 lakh): Life insurance premium receipts, PPF passbook, ELSS redemption or holding statement, home loan principal repayment certificate, children’s tuition fee receipts, NSC certificates.

• Section 80D: Health insurance premium receipts for self, spouse, children, and parents. For senior citizen parents not covered by insurance, actual medical expenditure up to ₹50,000 is deductible.

• HRA: Rent receipts for the full year, rental agreement, and landlord’s PAN if annual rent exceeds ₹1 lakh.

• Section 24(b): Home loan interest certificate from the lender.

• Section 80E: Education loan interest certificate.

• Section 80G: Donation receipts with the donee organisation’s 80G registration number.

• Section 80CCD(1B): NPS contribution acknowledgement for self-contribution up to ₹50,000 (over and above the 80C limit).

Foreign Income and Assets — Schedule FA, Schedule TR, Schedule FSI

This section is non-negotiable for any taxpayer who is a Resident and Ordinarily Resident (ROR) in India for FY 2025-26 and holds or derives income from foreign assets.

Schedule FA (Foreign Assets) requires disclosure of:

• Foreign bank accounts held at any time during the calendar year 2025 (not just financial year)

• ESOPs or RSUs granted by a foreign parent company, whether vested or unvested

• Foreign equity or debt investments

• Foreign immovable property

• Beneficial ownership or signing authority in foreign accounts

Schedule FSI covers foreign income earned during FY 2025-26. Schedule TR allows you to claim credit for foreign taxes paid on that income, to avoid double taxation. Collect the foreign tax return, TDS certificates, or withholding tax receipts before filing.

Important: Failure to disclose foreign assets under Schedule FA attracts a penalty of ₹10 lakh under the Black Money Act, regardless of whether the asset generates any income. This is not a technicality — it is a high-risk omission.

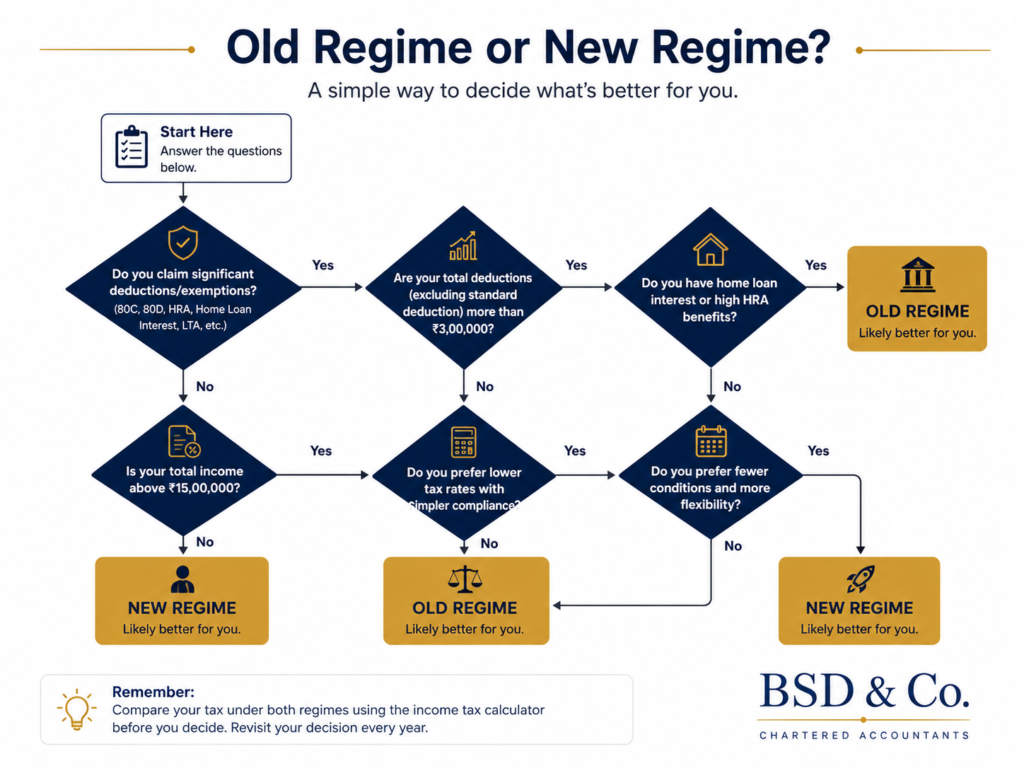

Choosing the Right Tax Regime – Form 10-IEA Mechanics

The new tax regime (lower rates, no exemptions / deductions) became the default regime from FY 2023-24. If you want to opt for the old regime (higher rates, but HRA, 80C, 80D, and other deductions available), you must explicitly choose it.

For salaried individuals: You can switch between regimes each year. Inform your employer of your choice at the start of the year for TDS purposes, but your final regime choice is made at the time of filing the ITR.

For business owners and professionals: The choice is more restrictive. Once you opt out of the new regime (using Form 10-IEA), you can return only once. After returning to the new regime, you cannot switch back to the old regime again (with limited exceptions).

The decision framework is straightforward: if your total eligible deductions under the old regime (80C, 80D, HRA, home loan interest, NPS, etc.) exceed a certain threshold — roughly ₹3.75 lakh for a ₹15 lakh income — the old regime remains beneficial. If not, the new regime’s lower rates deliver a better outcome. Run the calculation before filing.

Common Mismatches and How to Resolve Them

These are the most frequent mismatches we encounter at BSD during ITR season:

• AIS shows income not yours: Raise an online feedback on the AIS portal citing ‘Income of another person included’ or ‘Duplicate entry’. Retain proof. File your return based on correct income.

• TDS reflected in 26AS but not in AIS: Use Form 26AS as the controlling document for TDS credit. Excess TDS credit cannot be claimed unless it appears in Form 26AS.

• Capital gains in AIS differ from broker statement: Compute gains independently from your transaction history. If the AIS figure is incorrect, you can submit feedback. The ITR will accept your computed figure if supported.

• Interest income in AIS exceeds your records: Check whether all your FD accounts — including joint accounts and minor children’s accounts where you are the guardian — are included.

• Form 16 figures differ from salary slips: The most common cause is a mid-year salary revision where the TDS projection was not updated. Reconcile month by month.

When to File ITR-U (Updated Return) Instead

If you missed the original filing deadline (July 31), filed with errors, or need to add income omitted from a prior year’s return, an Updated Return (ITR-U) under Section 139(8A) is available.

ITR-U can be filed within two years from the end of the relevant assessment year — so for FY 2023-24 (AY 2024-25), the window closes March 31, 2027. However, filing an ITR-U attracts an additional tax of 25% (if filed within 12 months) or 50% (if filed between 12 and 24 months) on the additional tax payable.

ITR-U cannot be used to claim a refund, reduce tax liability, or increase a loss. It is strictly for increasing income disclosures and paying the resulting tax. If you suspect you have under-reported income in a prior year, consult your CA before the window closes.

How BSD Helps Clients File With Confidence

At B S D & Co., our pre-filing review process for each client involves a structured reconciliation of AIS, TIS, Form 26AS, and the client’s own income records before we prepare a single figure for the ITR. For clients with capital gains, foreign assets, ESOPs, or business income, we run a dedicated pre-filing review call.

Over 53 years of practice in Bengaluru, we have seen every variant of income complexity — from HNIs with multiple source portfolios to founders with foreign ESOPs and RSUs, to MNC employees with dual salary in two countries. The pre-filing checklist above reflects the systematic approach we apply for every client, every year.

Ready to file your ITR for FY 2025-26 without surprises? Book a pre-filing review with BSD. Call us at 080-4851 7108 or visit bsdgroup.in to schedule your appointment.